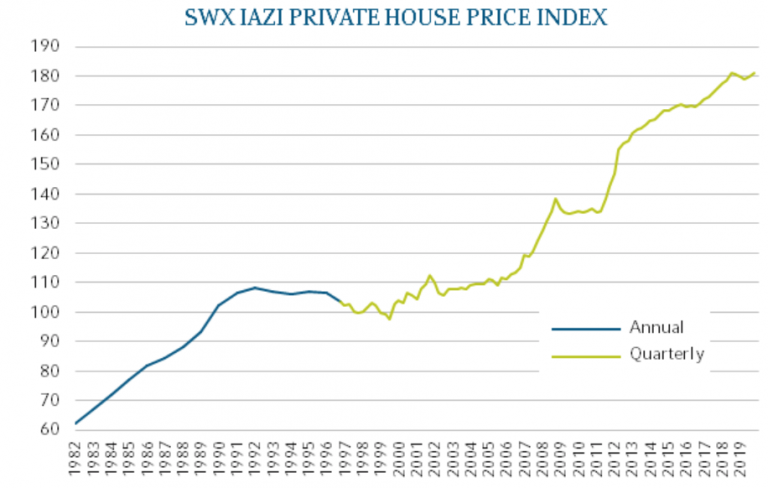

Every month, UBS takes a look at the current interest rate environment and provides a forecast for future developments. In the latest article on its website, the bank writes that with the current key interest rate of 0.50 per cent, we find ourselves in an environment of a slightly expansionary monetary policy. In 2023, inflation fell below 2 per cent, which corresponds to the SNB’s definition of price stability. This allowed the SNB to lower the key interest rate four times in 2024, most recently to 0.50 per cent. In view of the uncertain global situation and the diverging policies of the most important economic units, the question now arises as to whether the trend of falling interest rates in Switzerland will continue, whether a rise in interest rates is to be expected or whether there will be further easing.

UBS writes: ‘Yields on 10-year Swiss government bonds and mortgage rates with the same maturity stabilised in the first half of February after having risen significantly in January. In the second half of the month, however, there was a clear upward trend in bond yields again.’ Despite the still unclear situation in Ukraine and the potential impact of US tariffs on cars and pharmaceutical products, the risk of a fall in interest rates remains for Europe. For Switzerland, however, UBS expects that ‘in view of the low inflation in this country and the economic risks in the eurozone (…) the SNB will lower its key interest rates again. This should also limit the upside potential of longer-term interest rates. Yields on Swiss government bonds and mortgage rates are therefore likely to stabilise at the low levels seen in recent months. Mortgage rates linked to SARON are likely to benefit from a further interest rate cut by the Swiss National Bank.’

Long-term interest rate development in per cent

Based on these considerations regarding the initial situation, UBS has arrived at the following forecast for the long-term interest rate trend in Switzerland:

Sources: Bloomberg, UBS Switzerland AG. This is only an indicative interest rate. The effective interest rate is calculated using the margin + Compounded SARON of the accounting period. The Compounded SARON cannot be negative

avobis also expects interest rates to fall

In its latest analysis of interest rate trends in the most important international markets and in Switzerland, avobis is somewhat more cautious in its forecast for the time being. Although a further interest rate hike is obvious, ‘the SNB could nevertheless act more cautiously and pause.’

According to avobis, overall inflation in Switzerland fell to 0.40% in January, reaching a new low. This development is largely in line with expectations and is in line with the SNB’s forecast. Despite a supposed rise in the core inflation rate, price pressure remains low: in a monthly comparison, core inflation is slightly negative and the rise is primarily the result of base effects. There are therefore no signs of a turnaround in inflation – on the contrary, inflation is continuing to move towards zero. Inflation could already be at 0% or even in negative territory in the February data.”

National consumer price index: The chart shows the development of the national consumer price index (CPI) and the contributions of the core

contributions of the core inflation rate and the volatile components to the year-on-year change (avobis comment). Source of the chart: avobis, based on data from BfS

In its analysis, avobis therefore comes to the following expectation: ‘Against this backdrop, there are many arguments in favour of a further interest rate cut. Nevertheless, the SNB could tolerate temporarily low inflation, provided it remains within the target range in the medium term. In this case, a wait-and-see stance would be conceivable in order to preserve monetary policy room for manoeuvre for later interventions. Recent statements by SNB representatives at least indicate that such a strategy is not out of the question. This caution is also reflected in market expectations: forecasts for monetary policy easing have been scaled back for this year, while the interest rate swap curve has steepened significantly compared to previous months.’

Despite all the uncertainties and possible strategies of the SNB, avobis considers a key interest rate cut of 25 basis points to be the most likely scenario. However, a decision by the SNB to pause for the time being would not be surprising either.